No-insurance adjustments are discounted or negotiated self-pay rates that chiropractic providers offer directly to patients without insurance coverage. They exist outside insurance contracts entirely, which means uninsured patients can access care at rates far below standard chargemaster prices. For anyone paying out of pocket for spinal adjustments or post-accident recovery, understanding insurance-free adjustments is the difference between affordable treatment and a bill that stops care before it starts. Sparkmed offers a $25 chiropractic adjustment with no insurance required, making this one of the clearest examples of why use no-insurance adjustments matters in real practice.

Why use no-insurance adjustments instead of paying full price?

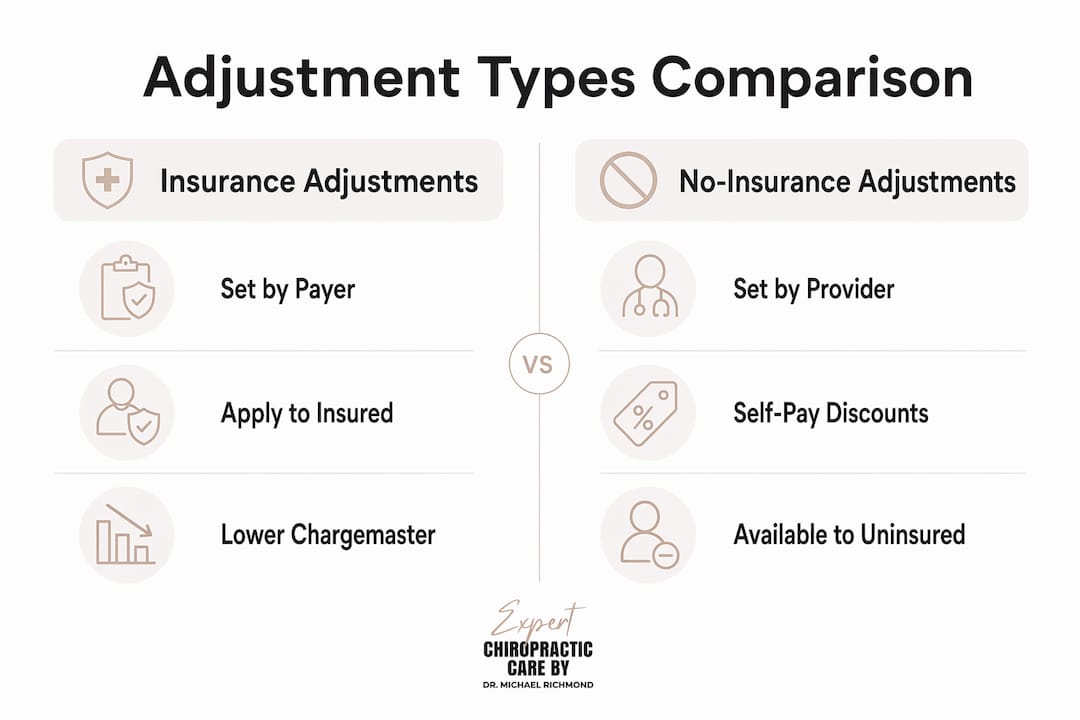

No-insurance adjustments exist because standard healthcare billing starts at chargemaster rates, which are the highest possible prices a provider can charge. Contractual adjustments are legally required write-offs of the difference between those chargemaster rates and the lower amounts insurance companies have negotiated. That write-off only applies when insurance is involved. Without insurance, a patient faces the full chargemaster price unless the provider separately offers a self-pay discount.

That is exactly where no-insurance adjustments come in. No-insurance adjustments are distinct self-pay or prompt-pay discounts offered outside insurance contracts to improve affordability and transparency for uninsured patients. They do not stem from insurer agreements. They come from provider policy and, in many cases, a genuine commitment to keeping care accessible.

The practical impact is significant. A chiropractic spinal adjustment billed at a chargemaster rate might be priced at several hundred dollars. A no-insurance adjustment can bring that same visit down to a flat, predictable rate. Transparent pricing backed by no-insurance adjustments reduces patient anxiety and supports treatment adherence, which means patients actually complete their care plans instead of stopping early due to cost.

Pro Tip: Before your first visit, ask the front desk directly: "Do you offer a self-pay or prompt-pay discount?" Most providers have a rate. Many just do not advertise it.

How do insurance contractual adjustments differ from insurance-free adjustments?

The word "adjustment" appears on almost every medical bill, but it means different things depending on the context. Knowing the difference protects you from misreading your balance.

Insurance contractual adjustments apply only when a provider is in-network with an insurer. Providers negotiate reimbursement rates with payers, and the resulting contractual adjustment is the amount the provider writes off because the contract forbids charging the patient more than the agreed rate. The provider never had a legal right to collect the full chargemaster amount under those contract terms. This is an accounting offset, not a favor.

No-insurance (insurance-free) adjustments work differently:

- They apply to patients with no active insurance claim on file.

- The provider sets the discount rate based on internal policy, not a contract with a payer.

- They are not legally mandated, though federal and state protections increasingly encourage price transparency.

- They can take the form of a flat self-pay rate, a percentage discount off chargemaster, or a prompt-pay reduction for patients who pay at the time of service.

The table below shows the core distinctions at a glance.

| Feature | Insurance contractual adjustment | No-insurance (self-pay) adjustment |

|---|---|---|

| Who sets the rate | Insurance carrier contract | Provider policy |

| Legal requirement | Yes, under payer contract | No, voluntary by provider |

| Who benefits | Insured in-network patients | Uninsured or self-pay patients |

| Billing trigger | Insurance claim filed | No insurance claim involved |

| Patient visibility | Shown on Explanation of Benefits | Shown on provider invoice |

Pro Tip: If you later file an insurance claim after receiving a self-pay rate, ask the billing department how that affects your balance. Reprocessing a claim can change your responsibility, sometimes upward.

Why are insurance-free adjustments important for affordability?

Uninsured patients face a structural disadvantage in healthcare billing. Without a contract between their insurer and the provider, they are technically exposed to the full chargemaster rate. The No Surprises Act, effective 2022, provides some protection by requiring providers to give Good Faith Estimates to uninsured patients before scheduled care. Patients can dispute bills that exceed those estimates by $400 or more through a federal resolution process. That protection matters, but it does not automatically lower the price.

No-insurance adjustments do lower the price. The benefits of no-insurance adjustments for uninsured chiropractic patients include:

- Predictable costs. A flat self-pay rate removes the uncertainty of insurance processing, deductibles, and co-insurance calculations.

- Faster access to care. No prior authorization is needed. Patients book, pay, and receive treatment without waiting for insurer approval.

- Reduced risk of surprise bills. When the provider quotes a self-pay rate upfront, the bill at checkout matches the quote.

- Better treatment adherence. Transparent upfront pricing reduces patient anxiety and makes it easier to commit to a full course of care.

- No network restrictions. Patients choose providers based on quality and location, not insurance network membership.

For patients recovering from a car accident in North Miami, these advantages are not abstract. Delayed chiropractic care after a collision worsens outcomes. A $25 flat-rate adjustment, like the one Sparkmed offers, removes the financial reason to delay. You can also read more about chiropractic cost saving strategies that work alongside self-pay pricing to reduce your total care expense.

How do no-insurance adjustments work in practice?

Understanding the process helps patients ask the right questions and avoid billing confusion.

- Ask before you book. Contact the provider and ask whether they offer a self-pay or prompt-pay discount. Get the rate in writing or by email before your appointment.

- Request a Good Faith Estimate. Under the No Surprises Act, uninsured patients scheduled for non-emergency care have a legal right to a written cost estimate before treatment.

- Confirm what the adjustment covers. Some providers apply the self-pay rate to the adjustment only. Others extend it to X-rays, exams, or follow-up visits. Clarify the scope.

- Pay at the time of service when possible. Prompt-pay discounts are often the deepest discounts available. Paying at checkout can reduce your rate further.

- Keep documentation. Save the quoted rate, the invoice, and your payment receipt. If a bill arrives later that does not match, you have a paper trail.

- Review your bill within 90 days. Medical bills can increase after initial postings due to claim reprocessing or coding reviews. Monitor any statements that arrive after your visit.

Financial assistance programs and charity care are different from no-insurance adjustments. Financial assistance programs differ fundamentally from contractual adjustments. Self-pay discounts are available to any uninsured patient who asks. Charity care typically requires income verification and a formal application. Do not assume you need to qualify financially to receive a self-pay rate.

Pro Tip: Combine a self-pay discount with a payment plan if the provider offers one. Many clinics will apply the no-insurance rate and then split the balance into monthly installments, making even multi-visit care plans manageable.

What are common misconceptions about insurance-free adjustments?

Several misunderstandings cause patients to either overpay or distrust their bills.

"The word 'adjustment' on a bill does not always mean money was removed in your favor. It can mean a contractual write-off, a self-pay discount, a billing correction, or a reprocessed claim. Read the line item description carefully before assuming your balance is final."

The most common misconceptions include:

- "An adjustment means I owe less than the original charge." Not always. Billing confusion can occur because "adjustment" can indicate a write-off, financial assistance, or a reprocessed claim that actually increases your balance.

- "No-insurance adjustments are the same as charity care." They are not. Charity care is income-based. Self-pay discounts are available to any uninsured patient who requests them.

- "All providers offer self-pay rates." Many do, but disclosure is not always required. Some providers only offer discounts when patients ask directly.

- "My bill is final after the first statement." It is not. Coding reviews or late-arriving insurance information can trigger a revised bill weeks later.

- "State laws protect me from all surprise bills." Federal protections under the No Surprises Act cover specific situations. State laws vary. Knowing your state's rules adds a layer of protection.

Approximately 7%–11% of insurance claims are underpaid below contracted fee schedules, often due to systematic errors like downcoding. This statistic matters for uninsured patients because it shows that even insured billing is error-prone. Uninsured patients who do not review their bills face the same risk of paying incorrect amounts.

How can uninsured patients get the most from self-pay pricing?

Maximizing the impact of no-insurance adjustments requires a few deliberate steps.

- Ask explicitly. Use the phrase "self-pay discount" or "prompt-pay rate" when calling a provider. Vague questions get vague answers.

- Compare rates across providers. Self-pay pricing varies widely. A quick call to two or three local clinics gives you a real market rate for the same service.

- Get everything in writing. A verbal quote is not a binding agreement. Ask for a written Good Faith Estimate or a printed fee schedule.

- Check billing statements line by line. Contractual adjustments must be properly documented and consistent. Any line item labeled "adjustment" without a clear description deserves a question.

- Know your rights. The No Surprises Act gives uninsured patients the right to dispute bills that exceed Good Faith Estimates by $400 or more. Use it if needed.

Patients who take these steps consistently pay less and experience fewer billing surprises. The role of no-insurance adjustments is not passive. It requires the patient to engage with the process. Providers who openly advertise their self-pay rates, as Sparkmed does, make that engagement far easier. You can also review transparent pricing benefits to understand how upfront rate disclosure protects patients from the start.

Key Takeaways

No-insurance adjustments are the most direct tool uninsured patients have to access affordable chiropractic care at predictable, transparent rates.

| Point | Details |

|---|---|

| Definition is distinct | No-insurance adjustments are self-pay discounts set by providers, not write-offs required by insurance contracts. |

| Ask to receive | Most providers offer self-pay rates but do not advertise them. Patients must ask explicitly to access the discount. |

| Federal protections apply | The No Surprises Act gives uninsured patients the right to a Good Faith Estimate and a dispute process for bills $400 over that estimate. |

| Bills can change | Coding reviews and claim reprocessing can alter a bill up to 90 days after service. Review every statement carefully. |

| Transparency improves outcomes | Upfront self-pay pricing reduces anxiety and increases the likelihood that patients complete their full care plan. |

What I've learned from watching patients navigate billing without insurance

Billing confusion is the single biggest reason uninsured patients stop chiropractic care before they recover. I have seen it repeatedly. A patient comes in after a car accident, gets a quote, then receives a bill three weeks later that looks nothing like what they expected. They assume the clinic made an error, or worse, that they were misled. Often, neither is true. The bill changed because of a coding review or a late-arriving document. But the damage to trust is real, and the patient stops coming.

The solution is not more legal protection, though the No Surprises Act helps. The solution is providers who publish their self-pay rates clearly, confirm them in writing at every visit, and explain what an "adjustment" line item actually means on a statement. Patients should not need a billing degree to understand what they owe.

No-insurance adjustments work best when both sides treat them as a formal agreement, not an informal favor. The patient asks, the provider confirms in writing, and the bill matches. That process builds the kind of trust that keeps patients in care long enough to actually get better. Sparkmed's $25 flat-rate adjustment is built on exactly that principle. The rate is stated, it is consistent, and patients know what to expect before they walk in the door.

— Spark

Affordable chiropractic care at Sparkmed, no insurance needed

Sparkmed is a chiropractic clinic in North Miami built around one principle: care should be accessible regardless of insurance status. The $25 chiropractic adjustment offer requires no insurance and no prior authorization. Patients recovering from car accidents or seeking ongoing spinal care get a clear, flat rate from the first call.

Sparkmed's billing team answers questions about self-pay pricing, payment plans, and what to expect on your statement before and after your visit. The clinic's accessibility commitment reflects a practice-wide standard for transparent, patient-friendly billing. Book an appointment or contact Sparkmed directly to confirm your self-pay rate before your first visit.

FAQ

What is a no-insurance adjustment in chiropractic billing?

A no-insurance adjustment is a self-pay discount a chiropractic provider offers to patients without insurance. It reduces the bill below the standard chargemaster rate and is set by provider policy, not an insurance contract.

Are no-insurance adjustments the same as insurance write-offs?

No. Insurance write-offs are legally required under payer contracts and apply only to insured patients. No-insurance adjustments are voluntary discounts providers offer to uninsured patients who ask.

Does the No Surprises Act protect uninsured chiropractic patients?

Yes. Under the No Surprises Act, uninsured patients scheduled for non-emergency care have the right to a Good Faith Estimate. They can dispute any bill that exceeds that estimate by $400 or more through a federal resolution process.

How do I ask for a self-pay discount at a chiropractic clinic?

Call the clinic before your appointment and ask directly: "Do you offer a self-pay or prompt-pay rate?" Request the rate in writing before your visit to avoid billing surprises.

Can my chiropractic bill increase after I receive a self-pay adjustment?

Yes. Coding reviews or late-arriving documents can trigger a revised bill up to 90 days after your visit. Review every statement and compare it to your original Good Faith Estimate or quoted self-pay rate.